Despite record European defense spending and new mechanisms for Ukraine support, the Alliance enters its summit shadowed by transatlantic mistrust and a US increasingly impatient with its allies.

- A Summit Rich in Data, Poor in Consensus

- From Spending to Capability: The Industrial Bottleneck

- Ukraine: Institutionalising the War Economy

- A Fractured Transatlantic Climate

- Regional and Global Implications

- Between Consolidation and Drift

- Europe is doing more spending more, producing more, and coordinating more

NATO’s annual summit in Ankara arrives at an uneasy moment for the Alliance. On paper, the picture is one of momentum: European allies are increasing defense budgets at their fastest pace in decades, industrial output is expanding, and a new financing mechanism for Ukraine has unlocked billions in coordinated support. Secretary General Mark Rutte is expected to present this as proof that long-standing American demands for burden-sharing are finally being met.

Yet the political backdrop tells a more fragmented story. A recent US military confrontation with Iran has sharpened tensions with European capitals reluctant to endorse Washington’s regional posture. President Donald Trump’s renewed frustration with allies amplified by disputes over territorial claims such as Greenland and public clashes with European leaders including German Chancellor Friedrich Merz—has injected volatility into what should be a carefully choreographed demonstration of unity.

The central question in Ankara is no longer whether Europe is spending more. It is whether quantifiable progress can still translate into political cohesion. Beneath the figures lies a deeper anxiety: that NATO is entering a phase where performance metrics are improving even as strategic trust deteriorates.

A Summit Rich in Data, Poor in Consensus

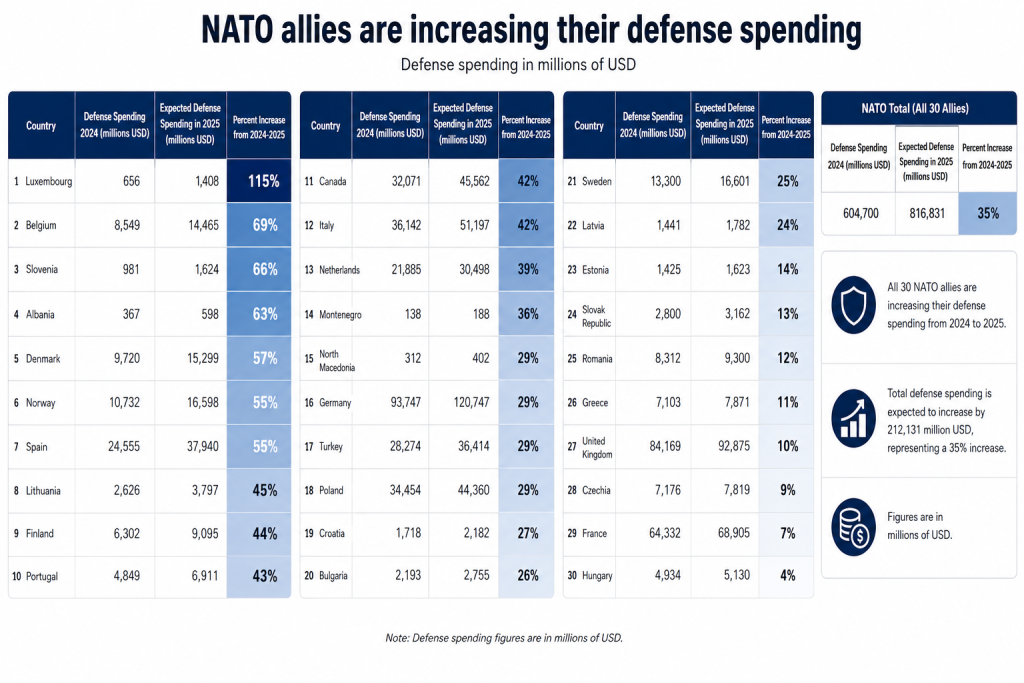

By traditional metrics, NATO’s story in 2026 is one of acceleration. European allies have moved faster toward a new long-term defence ambition of 5 percent of GDP—an extraordinary figure by historical standards, even if it remains politically elastic in its interpretation.

Northern and eastern flank states, including Lithuania, Denmark and Norway, continue to lead the charge, reinforcing a long-established pattern of frontline states driving Alliance readiness. What is more striking, however, is the broadening of effort. States previously criticised for strategic underinvestment are now increasing expenditure at double-digit rates. Even smaller economies, such as Luxembourg, are posting sharp percentage growth in defence budgets, signalling a political shift that would have been unlikely a decade ago.

The United States, by contrast, remains structurally dominant in absolute terms but lags in growth rate—a statistical reflection of its already vast defence base rather than strategic retrenchment. Still, in the current political climate, perception matters as much as arithmetic. In Washington, the narrative is not about burden-sharing improving, but about burden-sharing still not being enough.

This tension between data and perception is shaping the summit more than any formal agenda item.

From Spending to Capability: The Industrial Bottleneck

The second pillar of NATO’s messaging—defence industrial production—reveals both progress and constraint.

Europe’s rearmament cycle is no longer theoretical. Rising budgets are now feeding directly into defence firms across the continent. Germany illustrates the complexity of this transition: increased spending has not translated into a single-channel expansion of domestic primes, but rather a dispersed investment strategy spanning national industry, European partnerships, and external suppliers.

Elsewhere, procurement diversification is becoming a defining feature of the Alliance’s new defence economy. European states are increasingly turning to South Korea and Japan for advanced systems, reflecting both urgency and the limits of European production capacity. This outward-looking procurement model marks a subtle but important shift: NATO’s rearmament is globalised, not self-contained.

Perhaps most emblematic of this change is the rise of non-traditional defence actors. Firms such as Portugal’s TEKEVER, which has expanded rapidly in unmanned systems, illustrate how technological disruption is eroding the dominance of legacy defence contractors. The result is a more fragmented but more dynamic industrial ecosystem.

Yet fragmentation is also a vulnerability. NATO’s challenge is not simply producing more, but producing coherently—ensuring interoperability, supply chain resilience, and strategic alignment across increasingly diverse industrial actors.

Ukraine: Institutionalising the War Economy

If defence spending and industrial output represent NATO’s long-term rearmament, Ukraine represents its immediate operational test.

The Prioritised Ukraine Requirements List (PURL) has emerged as one of the most consequential innovations in Alliance coordination since the full-scale Russian invasion in 2022. By allowing European allies to finance US-produced military equipment for Kyiv, the mechanism effectively bridges Europe’s financial capacity with America’s industrial and technological edge.

With contributions surpassing $5.5 billion in under a year, PURL has become more than a logistical tool—it is a political instrument designed to stabilise transatlantic burden-sharing while sustaining Ukraine’s battlefield resilience. Norway’s leading role underscores the continued importance of smaller but strategically aligned NATO members in driving collective initiatives.

However, PURL also exposes structural dependence. Europe is paying more, but still relies heavily on US production lines for critical capabilities such as air defence systems, precision munitions, and advanced ISR platforms. This dependency is increasingly central to Washington’s strategic leverage within the Alliance.

In Ankara, discussions are expected to focus on formalising PURL into a more durable funding architecture. The underlying objective is clear: to prevent Ukraine support from becoming subject to annual political bargaining cycles in Washington and European capitals alike.

A Fractured Transatlantic Climate

Despite measurable progress on capability and financing, the political environment remains brittle.

The recent US confrontation with Iran has reintroduced strategic divergence between Washington and several European capitals, particularly over escalation management and regional stability priorities. European reluctance to fully endorse US operations has revived familiar tensions over strategic autonomy versus Alliance cohesion.

At the same time, President Trump’s transactional approach to NATO has intensified uncertainty. His criticism of European allies over burden-sharing is not new, but it is now amplified by broader disputes that extend beyond defence policy into territorial and diplomatic friction, including repeated tensions over Greenland and public exchanges with senior European leaders.

This convergence of crises—Middle Eastern instability, Arctic geopolitics, and intra-European political dispute has created what NATO officials privately describe as a “stacked stress environment.” The Alliance is no longer managing a single strategic challenge but multiple overlapping theatres of political disagreement.

Secretary General Rutte’s role in Ankara is therefore less about announcing new initiatives than about containing narrative divergence.

Regional and Global Implications

For Europe, the immediate implication is clear: defence spending increases are no longer sufficient to guarantee US strategic reassurance. The benchmark has shifted from effort to effectiveness, and from effectiveness to alignment.

For Eastern flank allies, particularly Poland and the Baltic states, the trajectory is broadly positive. Increased spending and industrial coordination strengthen deterrence against Russia. Yet these gains are contingent on continued US engagement, particularly in intelligence and high-end capabilities.

For the Indo-Pacific, NATO’s evolving procurement patterns and cooperation with South Korea and Japan signal a gradual but meaningful expansion of defence-industrial interdependence. This raises the possibility of a more globally integrated Western security economy—but also increases exposure to geopolitical shocks outside the Euro-Atlantic region.

At the institutional level, NATO faces a subtler risk: metric fatigue. As defence statistics improve, political cohesion does not automatically follow. The Alliance risks entering a phase where it can demonstrate capability gains but struggles to convert them into strategic confidence.

Between Consolidation and Drift

Over the next 6–12 months, three trajectories will shape NATO’s strategic direction.

First, defence spending is likely to continue rising across Europe, though political resistance will intensify in fiscally constrained economies. The sustainability of the 5 percent trajectory will depend on domestic political stability as much as external threat perception.

Second, industrial fragmentation will become a central policy challenge. Without coordinated procurement frameworks, Europe risks duplicating capabilities while still failing to close critical gaps in munitions and air defence systems.

Third, Ukraine support will remain the most immediate stress test. The evolution of PURL into a quasi-permanent financing structure could stabilise assistance flows, but only if US political consensus holds.

The principal risk for NATO is not collapse, but drift: a scenario in which measurable improvements coexist with declining strategic trust.

Europe is doing more spending more, producing more, and coordinating more

NATO’s Ankara summit encapsulates a paradox at the heart of the Alliance’s current moment. By almost every quantitative measure, Europe is doing more spending more, producing more, and coordinating more effectively than at any point in recent history. Yet these gains are unfolding against a backdrop of intensifying political friction between Washington and its European allies.

The result is a disconnect between capability and cohesion. NATO is becoming materially stronger while remaining politically fragile. For Secretary General Rutte, the challenge is not to prove that the Alliance is improving, but to persuade its members that improvement alone is enough to hold it together. In an era of overlapping crises and transactional geopolitics, that argument may prove harder to sustain than any defence budget target.