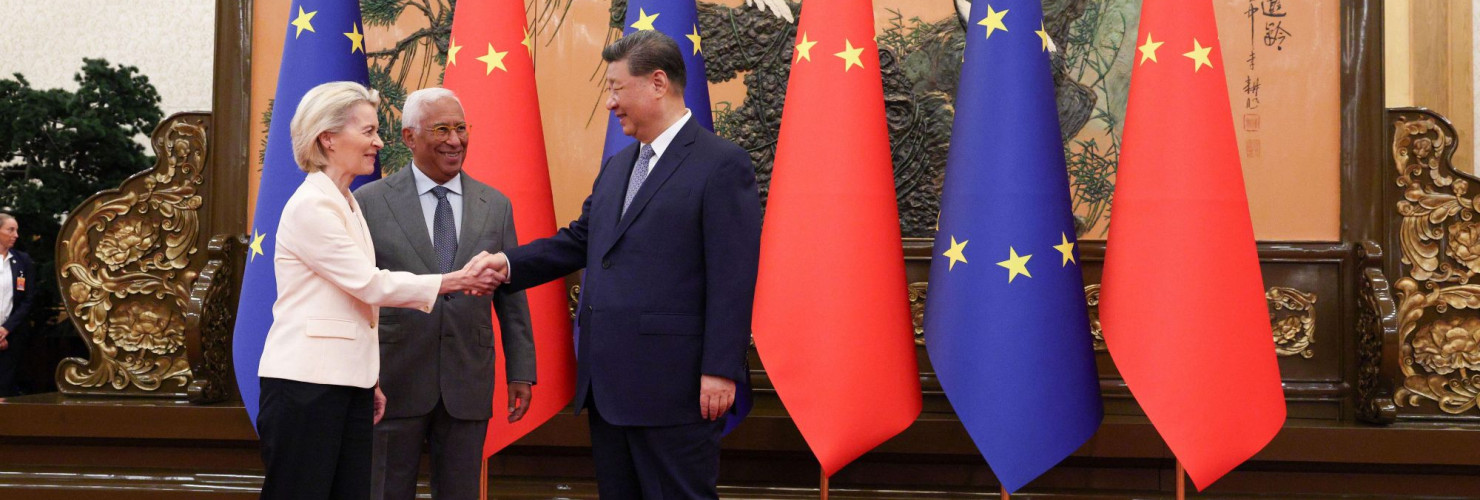

Europe does not simply “lack” a coherent China strategy. It is being actively prevented from having one by a country that has spent two decades building the dependencies, bilateral relationships, and institutional leverage to make sure it never could. The Chinese Commerce Minister arrives in Brussels this week. He knows this better than his hosts do.

On June 29, Chinese Commerce Minister Wang Wentao arrives in Brussels to meet EU Trade Commissioner Maros Sefcovic. The stated agenda is rare earths: China has been running an export licensing regime since late 2025 that has pushed prices for critical minerals used in European defence manufacturing and electric vehicles to six times their pre-restriction levels, with approval rates for European applicants running below 25 percent. Both sides will speak, publicly, of the need for “meaningful dialogue” and “concrete outcomes.”

Neither side is likely to get what it actually wants.

The deeper story is not about the meeting itself but about what the meeting reveals: that China has successfully positioned itself as the indispensable interlocutor in European strategic autonomy discussions — the gatekeeper of the very materials Europe needs to reduce its dependence on China. That paradox is not accidental. It is the product of a deliberate, long-run strategy whose sophistication Brussels has consistently underestimated.

THE ARCHITECTURE OF DEPENDENCY

The conventional framing of the EU-China relationship focuses on trade flows and headline deficits. The EU’s goods trade deficit with China reached €360.6 billion in 2025, growing 15 percent year-on-year, and has expanded a further 10 percent in the first four months of 2026. At roughly €1 billion per day, it is one of the largest bilateral trade imbalances in modern economic history.

But the deficit figure, while striking, is almost the least interesting thing about the relationship. More consequential is the structural architecture China has quietly assembled beneath it.

China controls 90 percent of global rare earth processing. It dominates tungsten (80 percent) and antimony (60 percent). Economists at the European Central Bank estimate that over 80 percent of large European firms sit within three supply-chain intermediaries of a Chinese rare earth producer. This is not a side effect of trade. It is an engineered chokehold, built patiently over two decades of below-cost industrial policy — and activated, with deliberate precision, whenever European trade policy moves in directions Beijing dislikes.

The 2025-2026 export control sequence was a demonstration, not an emergency. China applied just enough pressure to disrupt production at European carmakers and defence suppliers — factory utilisation cuts, temporary shutdowns, supply chain crisis meetings — without triggering the kind of escalatory spiral that would force European capitals to make a definitive choice about the relationship. The message was calibrated and clear: we can hurt you more than you can hurt us, and we can do it without anyone calling it a trade war.

“China applied just enough pressure to disrupt European production without triggering escalation. The message was calibrated and clear: we can hurt you more than you can hurt us.”

THE HUNGARY EQUATION

If rare earth leverage is China’s economic instrument, Hungary is its political one. This is not a metaphor. Budapest has, in the space of a decade, become the most important single node in China’s European strategy — and the EU institutions have watched it happen in slow motion, largely powerless to act.

The numbers are stark. China was Hungary’s largest source of foreign investment for the third consecutive year in 2025, accounting for 57 percent of total investment inflows. CATL’s €7.3 billion battery gigafactory in Debrecen began production in early 2026; BYD’s European passenger car plant, the first on the continent, reached mass production in the second quarter of the same year. The two plants represent not just investment but embedded industrial capacity inside the EU’s single market subject to EU rules on paper, but with supply chains, technology transfers, and strategic dependencies running back to Beijing.

The political consequence is structural. Hungary, armed with its Chinese investment portfolio and a veto in the European Council, has become a reliable spoiler of any EU approach to China that involves serious conditionality or genuine enforcement. Chinese Foreign Minister Wang Yi has called Hungary a “stellar example of a new type of international relations.” He means: an EU member state that reliably prevents the EU from acting like one when it comes to China.

This is not corruption or naivety on Budapest’s part or not only that. It is a rational calculation, heavily incentivised by Chinese capital, that aligning with Beijing on EU China policy generates returns that aligning with Brussels does not. Until that incentive structure changes, Hungary’s behaviour will not.

COLLATERAL DAMAGE BY DESIGN

The US-China trade war has added a third dimension to Beijing’s strategic position in Europe, and it is one that Beijing did not entirely engineer but has proved adept at exploiting.

The Trump administration’s tariff escalation in 2025 pushed Chinese exporters — in electric vehicles, steel, solar panels, chemicals, and consumer electronics — to redirect export flows toward the European market. Europe, with its relatively open trade regime and large consumer base, became the path of least resistance for Chinese overcapacity that could no longer reach the United States. China now accounts for roughly 30 percent of global manufacturing output while representing only 13 percent of global consumption; the difference has to go somewhere, and increasingly it is coming to Europe.

European firms describe themselves accurately as “collateral damage” in a dispute they did not cause. But the dynamic is not purely structural. China’s retaliation against EU de-risking efforts has been deliberately calibrated to exploit the gap between European trade policy rhetoric and European economic vulnerability. Mirror investigations, regulatory friction, selective supply chain disruption:

Beijing chose pressure points that affected the most economically exposed EU member states first, calculating correctly that their governments would brake any Brussels-led escalation before it reached genuinely costly territory.

The result is a European trade policy that is coherent in its ambitions the Industrial Accelerator Act published in March 2026, new steel tariffs from July, the Critical Minerals Sourcing Diversification initiative and incoherent in its enforcement. Every new defensive instrument Brussels reaches for runs into either Chinese leverage, member-state defection, or both.

“Europe has a trade policy coherent in its ambitions and incoherent in its enforcement. Every defensive instrument runs into Chinese leverage, member-state defection, or both.”

DE-RISKING IS NOT A STRATEGY

European Commission President von der Leyen’s formulation — “de-risking, not decoupling” — was always more communications product than strategic doctrine. It satisfied nobody completely: too confrontational for trade-dependent member states, too accommodating for those who believe Europe is being systematically outmanoeuvred. More fundamentally, it describes a direction of travel without specifying a destination or a mechanism for getting there.

De-risking from Chinese rare earth supply chains requires 20 to 30 years to build alternative processing capacity, according to industry estimates — timelines that span multiple Commission terms, multiple electoral cycles, and multiple Chinese export control cycles that will continue to shape European behaviour throughout. The RESourceEU joint purchasing initiative and the proposed EU Critical Minerals Centre are serious responses, but they are responses to a structural vulnerability that was allowed to deepen for two decades while European industrial policy remained deliberately neutral about supply chain geography.

De-risking from Chinese automotive competition requires confronting the reality that Chinese-owned plants are now inside the EU single market, producing batteries and vehicles under EU rules, with Chinese technology and Chinese strategic objectives embedded in their corporate governance. Tariffs applied at the border do not reach them. Competition rules were not designed for them. And EU member states — including Germany, whose carmakers depend on Chinese-origin battery supply — have powerful domestic reasons to resist the kind of regulatory tightening that would actually constrain them.

WHAT BRUSSELS DOES NOT WANT TO HEAR

The Wang Wentao visit on June 29-30 will be framed, publicly, as a step toward stabilisation. Both sides will confirm their commitment to dialogue. Sefcovic will press on rare earth licensing; Wang will offer enough movement to prevent escalation while extracting enough concessions to justify the trip to Beijing. A joint statement will speak of “constructive engagement” and “mutually beneficial outcomes.”

None of this is dishonest, exactly. But none of it addresses the structural problem.

The structural problem is this: China does not need a deal with “Europe.” It only needs deals with enough of Europe to prevent Europe from acting as a unified bloc. That threshold is remarkably low — one member state with a veto is sufficient. Beijing has that. It has invested €7.3 billion in a single Hungarian factory to ensure it keeps it. It has built supply chain dependencies that make European manufacturers involuntary advocates for accommodation. It has calibrated its coercive tools to produce maximum political friction inside Brussels without triggering the kind of visible crisis that would force European publics to pay attention.

The honest version of what European leaders should say, but will not, is this: China has a strategy for Europe. It has had one for years. It is working. Europe has an aspiration — de-risking, strategic autonomy, supply chain diversification — and a set of instruments that are systematically undermined by the very dependencies that aspiration is meant to reduce.

That gap between aspiration and architecture is not a policy failure. It is a strategic trap — one built with Chinese capital, maintained by European disunity, and scheduled to deepen, relentlessly, until someone in Brussels decides to call it by its actual name.

KEY FACTS AT A GLANCE

€360.6bn EU-China goods trade deficit in 2025, up 15% year-on-year 90% of global rare earth processing controlled by China 80% of large EU firms within 3 supply-chain steps of a Chinese REE producer (ECB) 6x price spikes for European critical minerals after China’s 2025-26 export controls 57% of Hungary’s total FDI inflows in 2025 came from China €7.3bn CATL battery gigafactory in Debrecen, Hungary (production from early 2026) June 29–30 Chinese Commerce Minister Wang Wentao visits Brussels for trade talks with EU’s Sefcovic